Accelerating the green energy transition

Surprising, but solar market again reached a new annual record of 18% growth, with 138 GW installed in 2020. Fortunately, global demand for solar installations did not shrink at all. Solar industry has managed a devastating global pandemic, despite the fact that COVID-19 has persisted longer than it was expected.

The global success of solar industry is due to many factors. One is its cost leadership, which continues to improve without an end in sight. Another is its versatility: solar covers a wide range of power applications from very small residential systems to very large utility-scale plants, individual installations to BIPV and integrated solar solutions in carports, apartment houses or agricultural green houses. There are also mobile PV systems and off-grid applications for rural electrification. More and more attention is paying to non on-grid applications – small scale PV, off-grid installations, mini-grids. It will be also a GW-scale markets with two-digit growth rates for the coming years. Finally, no other power plant can be planned and built as rapidly as any solar PV.

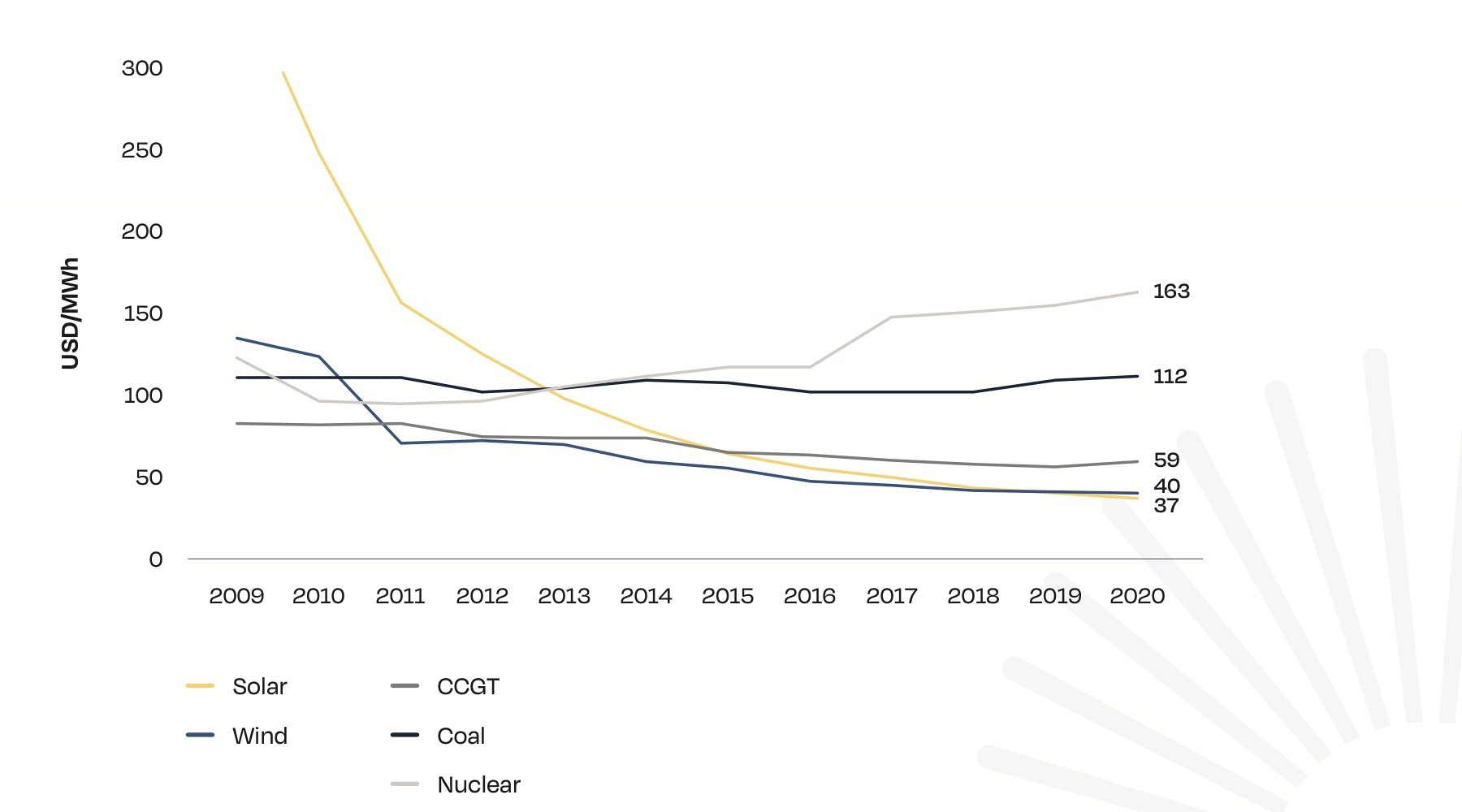

Solar electricity generation cost in comparison with other energy sources 2009-2020 (SolarPowerEurope).

The last solar market forecast by SolarPowerEurope sees much stronger growth for each of the coming years than anticipated earlier. The total solar power generation fleet will boost capacities from about three quarters of a terawatt in 2020, to over 1 TW in 2022, and nearly 1.9 TW in 2025, in most realistic scenario. The International Energy Agency (IEA), in its World Energy Outlook 2020 highlights that solar is the new king of electricity markets.

There are more markets that installed 1 GW per year than ever before. In 2018, only 11 countries were in the GW-club, which grew to 18 in 2020, and will reach 29 by 2023. It is obviously, that solar industry can grow fast under the right framework conditions. And many examples shows it (China, USA, Vietnam and so on). In addition, we have seen in the past and expect in the future double-digit growth also in the off-grid solar market (except for 2020, impacted by COVID-19).

It is certainly a nice that solar keeps surprising us with larger installation numbers, considering the fact that around 70% of global power still comes from non-renewable polluting energy and global carbon dioxide emissions are set this year for their second biggest increase in history. But solar power needs more global support from policymakers.

In the first half of 2021, the solar sector was characterized by increasing costs for wafer, cell, and module manufacturers, primarily due to rising silicon prices because of a supply shortage. COVID-19 affected several major solar markets, in particular India. Despite the various price increases along the solar value chain and the continued negative impact of COVID-19, solar will see another stellar growth year to 163.2 GW in 2021.

Solar’s cost improved for all segments with utility-scale solar now superior to fossil fuels in all unsubsidized investment cases, which also applies to solar + storage used to meet peak demand. The strength of solar was observed in many tenders in 2020, where winning bids in different geographical regions outperformed.

Solar PV Industry in Ukraine

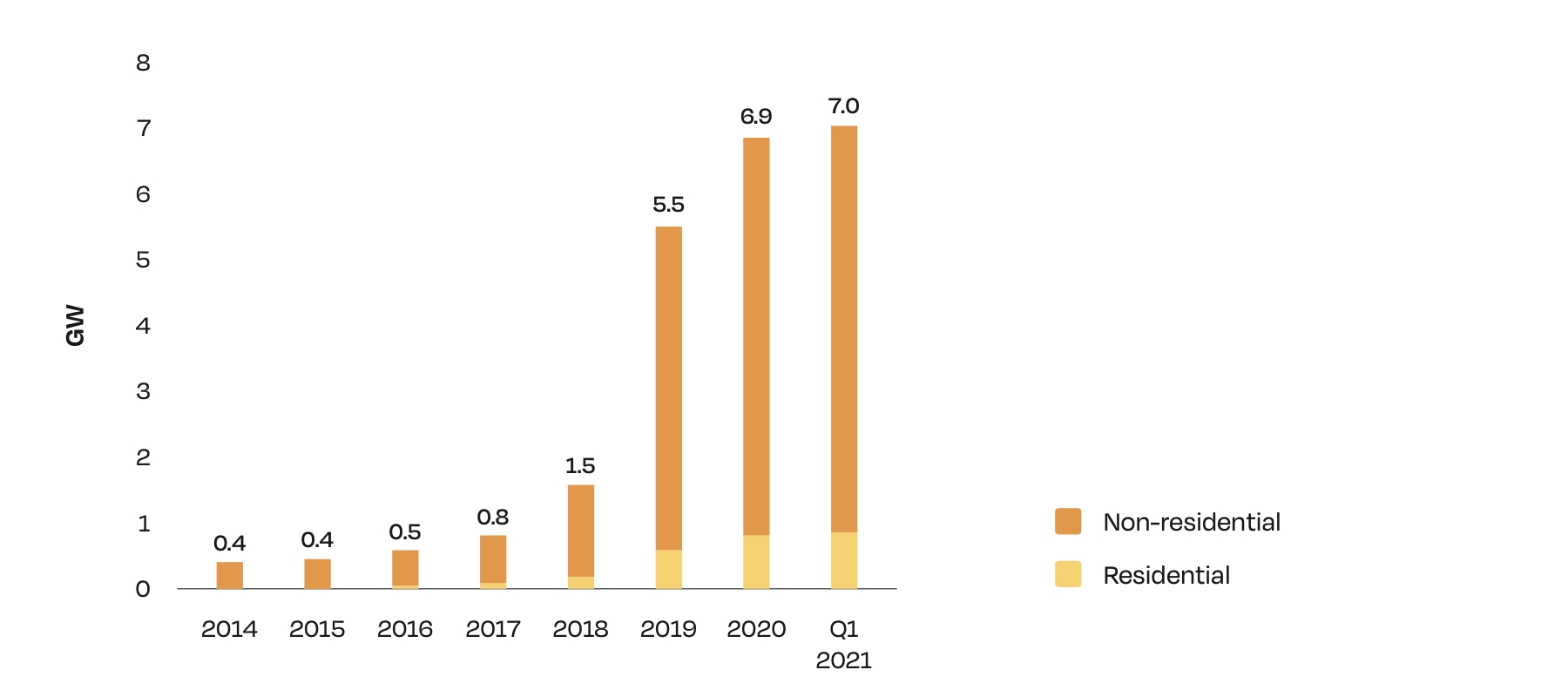

Intensive solar energy development in Ukraine began only recently, in 2018-2019, despite the fact that a feed-in tariff (FIT) for renewable energy support schemes was in place since 2010. In 2018, solar PV capacity reached 1,545 MW in total. The largest growth took place in 2019, when the total installed capacity increased 3.5 times compared to previous year. In 2020, the Ukrainian solar sector added 1,169 MW of commercial solar PV capacity and 226 MW of residential PV. In cumulative terms, 6,873 MW of solar was installed in Ukraine by January 1, 2021, with 779 MW or 11% of this capacity consisting of home PV (no larger than 30 kWac in size).

Installed capacity of commercial and private solar power plants in Ukraine (SolarPowerEurope, ASEU).

The main trigger for the development of solar generation in Ukraine was the FIT support scheme, which applies to all solar, wind and biogeneration facilities, but does not apply to hydropower plants and pumped hydro storage (except small and micro hydro power plants). The FIT tariffs in Ukraine are protected by the laws “On the Electricity Market” and “On Alternative Energy Sources” that guarantee an average payback period of 5,5-7 years for new solar systems. The FIT has stimulated the development of solar energy in recent years and led to the significant reduction of equipment costs in 2018/2019.

According to law amendments introduced in the middle of 2019, the auction support system should have already been implemented for new RE projects, substituting the FIT support scheme. The “pilot” auction should have taken place in December 2019 and the regular auctions should have started from January 2020. But the government has not yet announced the support quotas for 2020/2021 auctions and for the future, and has postponed the start of auctions.

The key challenges that the Ukrainian solar sector faces include a lack of trust from the investor’s side in the government’s activities in the RE sphere, huge debts for purchased electricity, the ongoing international arbitrages around retroactive FIT cuts and the possible implementation of an additional excise duty for renewable energy in late 2021. Moreover, the impact of COVID-19 to the economic context in Ukraine and the high costs of loans for residential PV are significant new obstacles for the development of the industry, as well as the decreasing investment climate.

Due to the uncertainty about the future of retroactive changes for PPAs and problems with auctions, investments in new PV reduced significantly in 2020 compared to 2019. This also caused significant job losses for the local solar industry – more than 5,000 employees left the industry. The government’s hard stance on renewable energy added to the prolonged difficulties foreign investors had in carrying out their business due to travel restrictions. All this will lower foreign investments considerably.

Once the RE auction support scheme is launched, it will lead to a next growth phase for the utility-scale PV segment, but not earlier than in 2022-2025. The further development of BESS is also necessary even for achieving the unambitious 25% RES goal by 2035, and for further renewable development. An appropriate law to solve this issue is still under consideration at the Parliament energy committee since 2019.

In the coming years, a slowdown is set to take place in the development of all new renewables in Ukraine, unless the government improves the framework conditions for new investments in the PV sector. Taking into account global trends it is necessary to be more ambitious when it comes to solar development with more support from policymakers, in order to implement better policy frameworks that enable solar to reach its full potential.

Source: SolarPowerEurope, ASEU

Read more:

Photovoltaics: prospects and opportunities in Ukraine

On the problems of the formation of the solar energy industry - in an interview with Dmytro Lukomskyi, Ph.D., an expert in solar energy.

What does solar energy expect in 2019?

According to the analysis of previous reports on the results of 2018, solar energy has demonstrated itself in the best way among all types of RES, lending its development potential to the current year.

Internal opinion regarding Ukrainian PV market

Solar energy market in Ukraine is going through a stage of rapid growth. Read the interview with Dmytro Lukomskyi.

Warehouse logistics in Ukraine

Warehouse logistics is a promising area of investment. There is a shortage of high-quality Class A warehouses and specialized hubs in Ukraine.