Local Expertise | Practical Experience

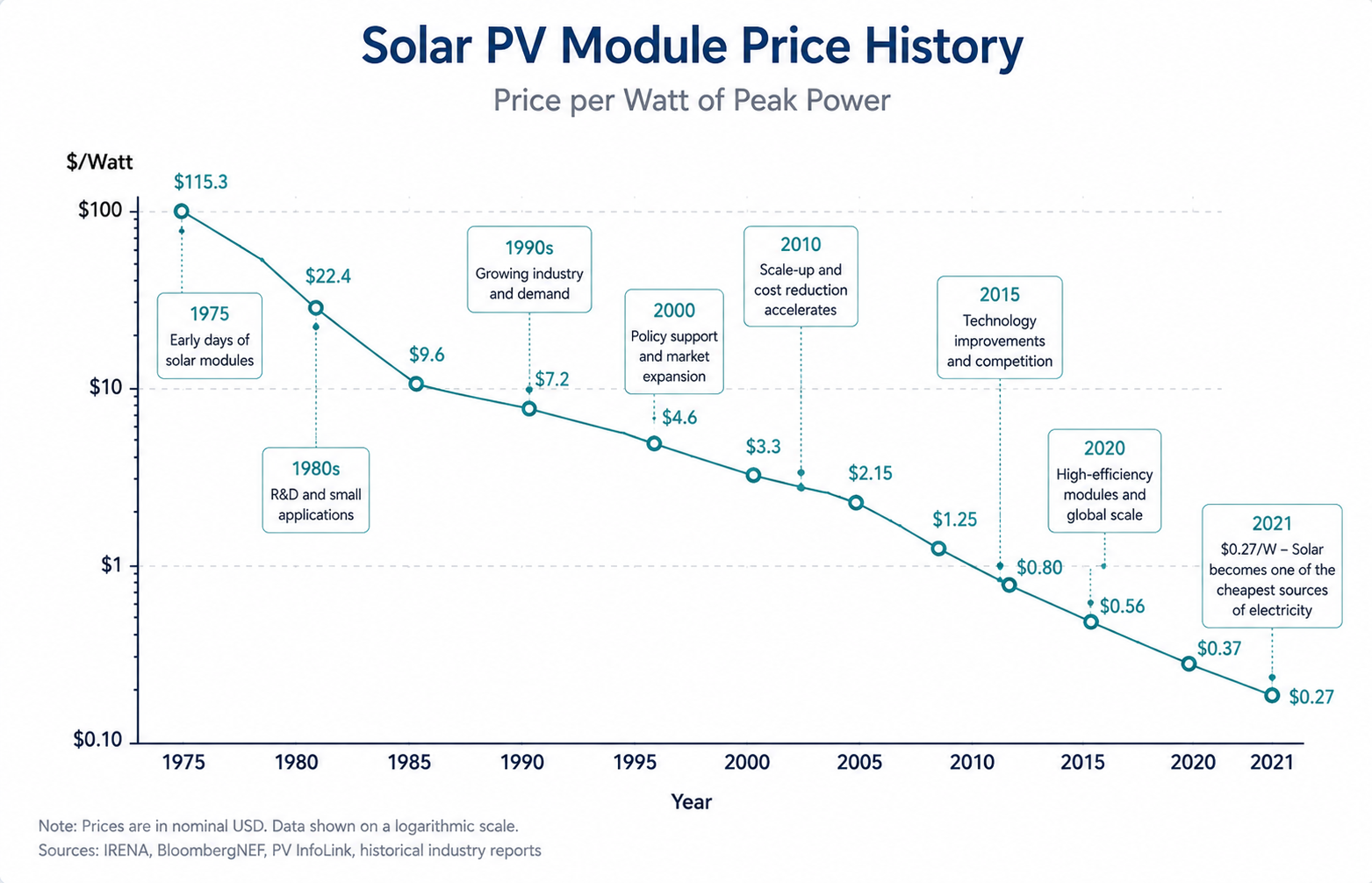

Over the past five decades, solar photovoltaic technology has undergone one of the most remarkable cost reductions in industrial history. Module prices have fallen from more than USD 100 per watt in the mid-1970s to historic lows today, transforming solar power from a niche technology used primarily in space applications into one of the world’s most affordable sources of electricity.

This dramatic decline has been driven by technological innovation, economies of scale, government support, and continuous improvements in manufacturing efficiency. This article explores how photovoltaic module prices evolved over time, what factors contributed to this transformation, and why solar energy continues to become increasingly competitive worldwide.

Figure 1. Historical decline in solar PV module prices (logarithmic scale).

Today, utility-scale solar PV is one of the lowest-cost sources of new electricity generation in many regions of the world, often outperforming conventional coal, natural gas, and nuclear power on a levelized cost basis. This represents one of the most significant technological and economic transformations in the history of the global energy sector.

What has contributed to such a rapid reduction in technology costs?

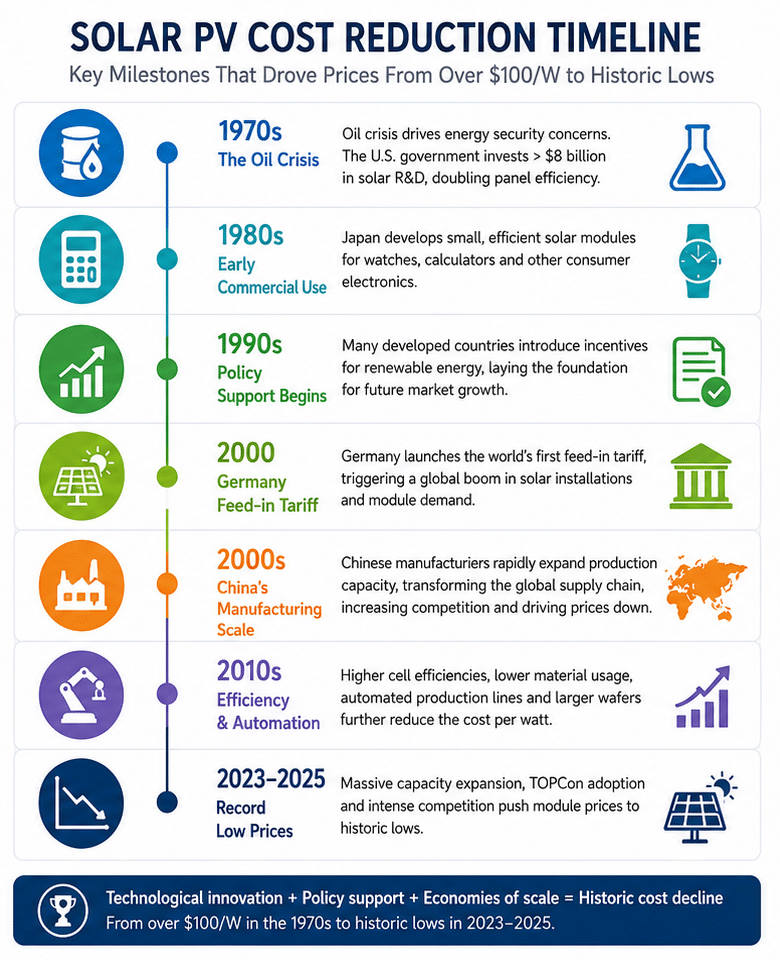

The First Driver: The 1970s Oil Crisis

In the 1970s, the world faced an oil crisis. This led to increased pressure to research and develop alternative energy sources. The US federal government allocated more than $8 billion to research and development of solar energy technology. As a result of this programme, the efficiency of solar panels doubled. A process began whereby increased production of modules led to a reduction in their cost.

After the programme ended, it was the Japanese who continued to work in this area. By the end of the 1980s, they had developed small but relatively powerful modules for powering watches, calculators, etc.

Despite these technological advances, the global photovoltaic market remained relatively small throughout the 1980s, with applications primarily limited to satellites, telecommunications, and specialized off-grid systems.

Government Incentives and China’s Manufacturing Scale

In many developed countries, the process of introducing economic incentives for the use of renewable energy sources (RES) began in the mid-1990s. But the most influential was the feed-in tariff policy introduced in Germany in 2000. The German government promised to pay renewable electricity producers twice the market price for 20 years.

There was a boom in the installation of solar capacity. Demand for solar panels increased – the more they were produced, the cheaper they became.

The industry’s next major turning point came when Chinese manufacturers rapidly expanded production capacity during the 2000s, transforming the global photovoltaic supply chain. Their rapid growth intensified global competition, accelerated economies of scale, and drove module prices down dramatically.

This created a powerful virtuous cycle: technological progress reduced costs, lower prices stimulated demand, higher demand encouraged additional manufacturing investment, and increasing production volumes drove costs even lower.

Many countries around the world began to introduce legislation that stimulated the development of the renewable energy market, including Ukraine, which introduced a mechanism of state support for the industry through a feed-in tariff in 2009.

Within just five decades, photovoltaic technology evolved from an expensive niche solution used primarily in space exploration into one of the world’s most competitive sources of electricity.

However, the story did not end there. Between 2023 and 2025, the photovoltaic industry entered another period of rapid transformation, with module prices reaching their lowest levels ever recorded.

Figure 2. Key milestones in the long-term decline of solar PV costs.

The New Era: Record Low PV Module Prices (2023–2025)

The photovoltaic industry entered a new phase between 2023 and 2025. Following the temporary increase in prices caused by supply chain disruptions during the COVID-19 pandemic and the global energy crisis, module prices declined faster than many analysts had anticipated.

The primary driver was the rapid expansion of manufacturing capacity, particularly in China. New production lines for polysilicon, wafers, cells, and modules came online simultaneously, creating significant oversupply across the entire PV supply chain. As manufacturers competed for market share, module prices reached their lowest levels in history.

At the same time, the industry completed another major technological transition. TOPCon (Tunnel Oxide Passivated Contact) solar cells rapidly replaced conventional PERC technology, offering higher conversion efficiencies without substantially increasing manufacturing costs. Larger wafer formats, higher module power ratings exceeding 700 W, and continuous improvements in manufacturing automation further reduced the cost per installed watt.

Lower equipment prices accelerated investment worldwide. According to the International Energy Agency (IEA), the sharp decline in module prices during 2023 significantly contributed to record global solar deployment, making utility-scale photovoltaic projects the lowest-cost source of new electricity generation in most regions of the world.

Although exceptionally low prices placed considerable financial pressure on many manufacturers, they also reinforced one of the industry’s defining characteristics: continuous cost reduction driven by technological innovation and economies of scale.

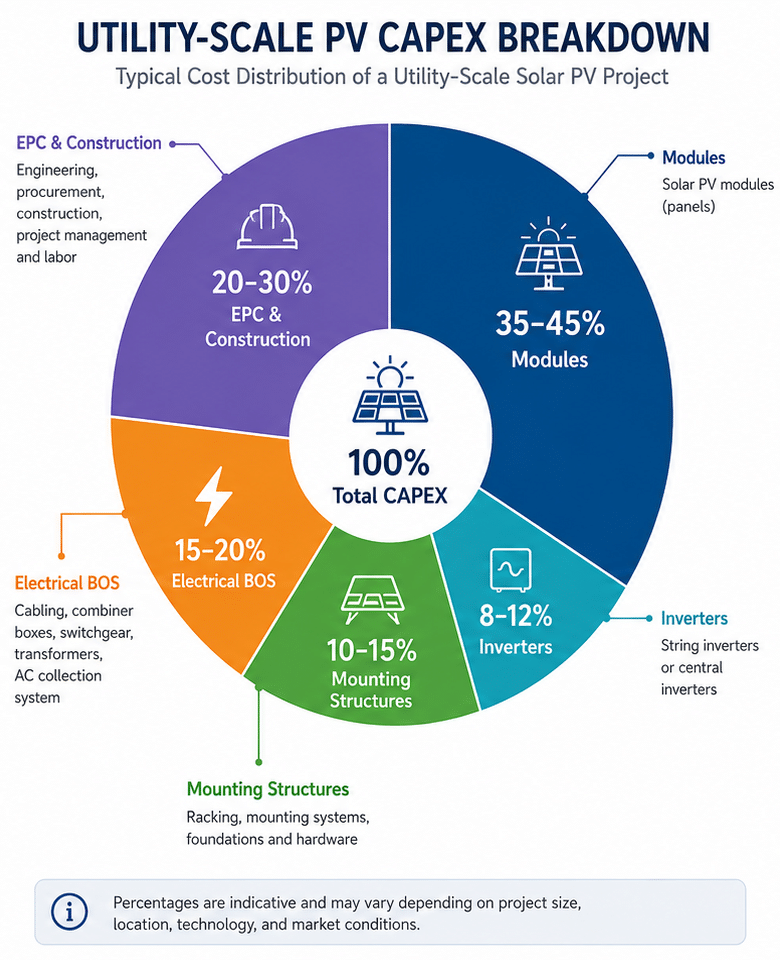

Evolution of Utility-Scale PV CAPEX

While photovoltaic module prices receive the greatest attention, they represent only one component of the total investment required to build a solar power plant.

Figure 3. Typical utility-scale PV CAPEX distribution. Actual shares vary by project size, technology, location, and market conditions.

The capital expenditure (CAPEX) of a utility-scale PV project includes solar modules, inverters, mounting structures, DC and AC electrical equipment, cabling, transformers, civil works, engineering, procurement, construction (EPC), grid connection, and commissioning.

Over the past two decades, every major cost category has experienced significant improvements.

Higher module efficiencies have reduced the number of modules, mounting structures, cables, and installation hours required to achieve the same project capacity. Modern string inverters have become more powerful, reliable, and cost-effective. Mechanical structures have been optimized for larger modules, while digital engineering tools and standardized construction practices have improved installation productivity.

As a result, today’s utility-scale solar plants require substantially lower capital investment per installed megawatt than projects built only a decade ago. According to recent international market data, utility-scale PV system prices in several mature markets have fallen to approximately USD 0.3–0.6 per watt, depending on project size, location, and local market conditions.

This decline in total system cost—not only module prices—has been the key factor behind the dramatic reduction in the levelized cost of electricity (LCOE) from solar PV.

Will Solar Continue to Get Cheaper?

Although the pace of cost reduction is unlikely to match the extraordinary declines observed during the past two decades, further improvements remain highly probable.

Several technological trends are expected to continue lowering the cost of solar electricity.

- First, ongoing improvements in cell efficiency—including TOPCon, heterojunction (HJT), back-contact (BC), and future tandem cell technologies—will enable greater energy production from the same installation area.

- Second, manufacturing processes continue to become more automated and efficient, reducing material consumption and production costs.

- Third, larger and more powerful modules reduce balance-of-system costs by requiring fewer electrical connections, mounting components, and installation hours per megawatt installed.

- Finally, project optimization through advanced software, digital monitoring, artificial intelligence, and improved construction techniques continues to increase overall project efficiency.

- Future cost reductions may become less dramatic than those seen in previous decades, and short-term price fluctuations will continue to occur due to raw material costs, trade policies, and supply-demand cycles. Nevertheless, the long-term trend remains clear: solar photovoltaic technology continues to become more efficient, more reliable, and more cost-effective.

The International Energy Agency expects solar PV to remain the fastest-growing renewable generation technology worldwide throughout the remainder of this decade, supported by continued technological progress and strong global investment.

Avenston’s Practical Perspective

Since 2010, Avenston has participated in the rapid evolution of the photovoltaic industry, witnessing first-hand one of the most remarkable technological transformations in modern energy.

Over the years, our engineering teams have worked with several generations of photovoltaic technology—from early polycrystalline modules with power ratings below 250 W to today’s high-efficiency TOPCon modules exceeding 700 W. Alongside this evolution, we have seen substantial improvements in inverter technology, mounting systems, engineering software, construction methods, and project management practices.

These advances have transformed not only equipment prices but also the overall economics of utility-scale and commercial solar power plants. Higher energy yields, lower installation costs, improved reliability, and more efficient operation have collectively reduced the lifetime cost of solar electricity to levels that were difficult to imagine only fifteen years ago.

This long-term industry experience provides valuable practical insight into how technological innovation, manufacturing scale, and engineering optimization have worked together to make photovoltaic energy one of the world’s most competitive sources of electricity and a cornerstone of the global energy transition.

Read more:

Photovoltaics: prospects and opportunities in Ukraine

On the problems of the formation of the solar energy industry - in an interview with Dmytro Lukomskyi, Ph.D., an expert in solar energy.

Alternative draft laws on auctions for support of renewables in Ukraine

Please be informed that following the registration on 7 June 2018 by a number of members of the parliament, including Acting Head of Fuel and Energy Committee of the Ukrainian Parliament Oleksandr Dombrovskyy.

Summary of Draft Law on Renewable Energy Auctions

Draft Law introducing new support system for renewable energy projects in Ukraine has been registered with the Parliament on 07 June 2018 under registration number 8449.

Interview with Dmytro Lukomskyi to Solar Academy

Solar Academy, a professional school in the field of solar energy, interviewed the Chief Executive Officer, who noted the relevance of optimization work of solar power plants.